With a focus on underperformers, the stand-out this month in the UK Legacy Banks category is HSBC and what appears to be their obliviousness to the decline in their app’s performance. Despite this being a big problem for HSBC, we see no evident improvement in sight.

Does HSBC even care? Or are they just relying on their grandiosity?

This type of performance is so far below the expected standards of a Legacy bank and we are baffled by what we are seeing. As Tony explains in the June snapshot, the trend is quite out of the ordinary in comparison to banks of a similar ilk.

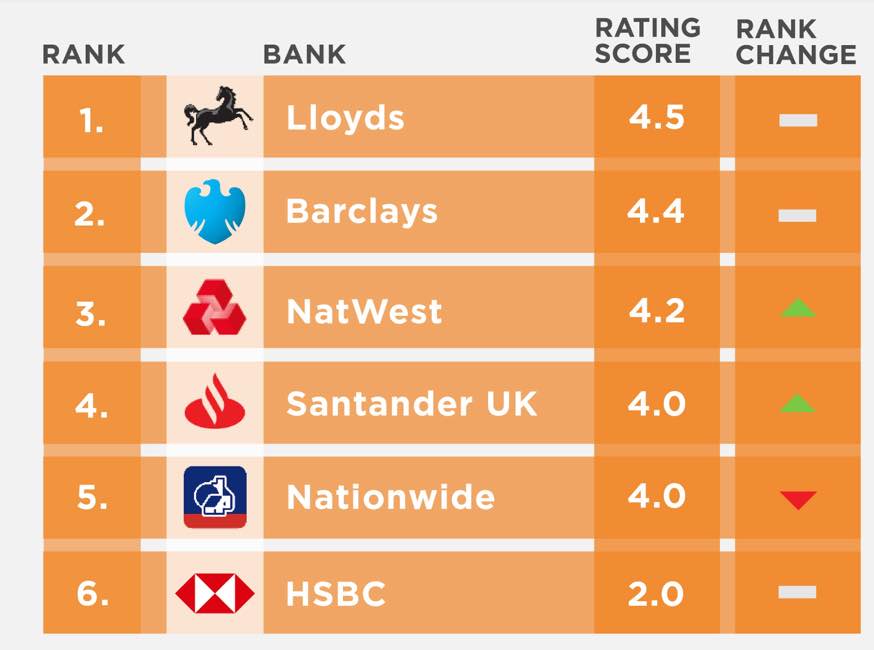

Sporadically, we do see a slight improvement, but with an Engaged Customer Score (ECS) of just 1.5 HSBC almost has the lowest score they could get, and sentiment on churn risk is over 10x that of Lloyds.

Using SURF analysis Tony shows the impact of what is going on and identifies the fundamentals of what HSBC should be addressing at a basic level if they’re going to see improvement, and if they are to make any real impact on churn.

With problems across the board, HSBC are not even close to meeting customer expectations.

Has HSBC given up even trying? Were they ever trying in the first place? Tell us what you think.

If you would like a personalised look at your own bank's performance, contact Touchpoint Group today and we can organise a specific insights session just for your business.

Video Segments

Intro – 00:00:00

Engaged Customer Score Performance – 00:01:19

SURF Analysis: HSBC – 00:03:17

HSBC Churn Rates – 00:04:28

HSBC Customer Reviews – 00:05:49

Conclusion – 00:06:34

Full Transcripts

00:02 Glenn: Hello everybody and welcome back to another Banking App Insight session: Legacy banks in the UK for June of 2022. And boy, oh boy! As you would expect with these sorts of banks the vast majority of them duking it out at the top with fairly good customer experience and engaged customer scores, but there is one big elephant in the room, and that is HSBC. My God.

We look at some of the other banks and some of the other segments, and you can see the sort of ‘Whack-A-Mole’ approach of some gains, some going backwards, some gains again and then going backwards as they are trying to fix problems. But, HSBC just continue the decline in underperformance, there is no real improvement in over a year.

So, this is a multi-billion dollar problem with people threatening to leave and you have to ask, ‘Are they committed to that customer experience? Or are they just letting it ride?’

I'll pass it over to you and let's have a look.

01:05 Tony: Great. Thanks Glenn. As you mentioned, there are a lot of good performers in the UK. But, today we will focus on HSBC, and this first chart will show you why.

What we have seen is often there are some banks, they have a problem, they may take a few months to fix it, but if we look at the top here. There's a few duking it out at the top here on this Engaged Customer Score. If you recall the Engaged Customer Score are those giving a comment and a score. We find that's really the pointy end. If you're on top of this score you can actually see things as they happen, and your scores are real movements in the quality of your app.

So, what we're seeing here is at the moment Lloyds is on top, but in the past we have got things of the likes of Barclays up there as well, and even the likes of Nationwide. Although Nationwide have improved over the past six to eight month, they're on a bit of a decline over the past two months. But it looks like nothing in comparison to what the story is for HSBC. So, this is in red at the bottom here.

One of the things you can see is there was a decline happening at least a year ago. There were some problems going on there. Looks like they attempted to fix a few things. They got better, but it looks like from December there was - I don't know what the story is inside HSBC, but it seems as they are like. ‘Well, we've given up. We're not going to attempt to even try to fix these things, let's let it drop away’.

And it seems to have dropped away from that December point, it was sitting at around 2.5. The average score now is 1.5 and I have mentioned in other sessions here that the lowest possible score you can get is 1. That is If everyone gives you a score of 1. But, 1.5 is getting pretty much close to that.

There seems to be some improvement in May and June, but that's not enough. Again, the speed of this from a customer advocate, this means a whole year of inactivity from these customers. And obviously churn is part of that story.

Let me jump in and show you the impact of what is going on inside here. One of the familiar views you might have seen before is this SURF analysis which is around the fundamentals you need to get right for your app to be working at a base level, the foundations. That's Security and logging in, the Usability, the Reliability, and the Functionality.

Across the board here, you can clearly see what stands out here. If we look at Reliability on the left there, basically one half of customers are talking about your app being unreliable. This is actually all negative things. Being high is pretty bad.

And one half of customers saying that they are unreliable. If we compare to some of the leaders like Lloyds at 6.7%, it's just a massive difference you can't even compare. It looks like HSBC are sort of working in a different world here. One of the problems of course, this is across the board. I'm not going to solve their problems in this short conversation here, but we have a look at the impact of what's going on.

There are problems across the board everywhere. But, let's have a look at one of the first pictures we can see here.

In conversations that customers, the feedback they give, they will talk about leaving or moving, in its various forms. What we can see here is the percentage of people talking about that. If you recall that very first chart where we saw the HSBC score declining, this pretty much reflects that same movement, but in the opposite direction of course. In June last year we saw 1.5% of customers mentioned something about churning or leaving HSBC.

Of course, even though these numbers reached a high point of 6% in April this year they have dropped, but they're still sort of 4% at that level, and you might think, ‘Well, that's not that high, is it, at 4%?’ Well, we've got to consider that not everyone actually says that in their conversation. They are not actually all going to say, "I'm going to leave” but, in their heads they probably are thinking about leaving.

Now, is that high? Is 6% and 4.5% high? Well, let's have a quick look here across some other banks.

Churn is mentioned by others but, if we compare it to this just in June, by the way, at 4.1% of customers talking about that. We see Lloyds is at 0.3%, just about nothing. A handful of people talking about it, at 1.2% for Nationwide.

So again, HSBC is in a league of its own and it's having actually a strong impact on customers. If we look at the right here at what's happening, and these are just the direct comments of people talking about threatening churn. We're getting for example here, "I moved bank because of the problems with the app after nearly 50 years with them". "Frustrating enough to consider switching a bank with a functional app". "It should be easier changing banks", and: "my advice is to switch banks immediately", "Switched banks to a modern one so I can actually use my money". These things like that, that's a massive problem. So, anyone in here who wants to use the app as their main channel is having a major issue, and they're actually saying they're leaving.

I'd imagine in the numbers for HSBC, they're probably seeing similar things. A massive problem for HSBC. They need to fix this, they need to go basics and get this right.

Thank you Glenn.

06:40 Glenn: Yeah. So, HSBC - Anyone there, if you're watching this, pull your socks up, my friends. Feel free to reach out and we can help you to get a little deeper in regards to what needs to be turned around.

Thanks, folks. Feel free to share and reach out to us if you want to have a chat.